After the FDA approved Palynziq (formerly pegvaliase) for use in adults with phenylketonuria (PKU), a rare genetic disease, this week,�BioMarin Pharmaceutical�(NASDAQ:BMRN)�is in a great position to add hundreds of millions of dollars in new revenue to its top line. BioMarin already markets one PKU therapy, Kuvan, so it should be able to hit the ground running. Is BioMarin a stock worth buying now?

What is PKU?A genetic disease caused by an inability to break down an amino acid, PKU can result in the toxic buildup of phenylalanine in the brain, particularly if patients consume�protein-rich foods or foods containing aspartame, an artificial sweetener.

IMAGE SOURCE: GETTY IMAGES.

As phenyalanine levels increase to dangerous levels, it can cause irreversible brain damage, developmental delays, and neurological problems, including seizure. It's a severe condition, but it's relatively rare. Globally, it impacts about 50,000 people.�

Because PKU is debilitating, all 50 states in the U.S. require PKU screening at birth. There's no cure for PKU, so treatment involves a lifelong dietary restriction that's very hard for patients to comply with. In�some PKU patients,�BioMarin's Kuvan, a pharmaceutical version of BH4, a natural substance that reduces phenyalanine levels by breaking it down, is also prescribed.

Currently, only about 12% of PKU patients, most of whom are children, take Kuvan, yet it's BioMarin's second best-selling product, with $408 million in sales in 2017.

Reaching more PKU patientsPalynziq is a potent drug, and because of this, it's initially only being approved for use in adults with PKU. BioMarin believes roughly 12,000 adults in the U.S. could benefit from using its newly approved drug and that its worldwide addressable market totals about 33,000 people.�

An enzyme replacement approach, Palynziq substitutes the deficient phenylalanine enzyme in PKU with a version of the enzyme phenylalanine ammonia lyase, which can break down�phenyalanine.�

Immune responses, including anaphylaxis, occurred in Palynziq's trials, so the FDA approval includes a REMS program, and the dosing of it in patients will be titrated over four to six months to improve tolerability and so that patients can take the lowest effective dose. In trials, 11% of patients discontinued Palynziq because of adverse reactions.�

While safety concerns can't be ignored, Palynziq is a first-of-its-kind solution for adult patients, and its efficacy could allow BioMarin to treat substantially more PKU patients than Kuvan. According to BioMarin's management, Palynziq has billion-dollar per year peak sales potential.

Initially, BioMarin's focus will be converting the 200 adult PKU patients that participated in Palynziq's trials into commercial users. Once that's done, the company will focus on the 2,300 adult Americans who are being treated in clinics, and then, it will embrace a strategy to reach the roughly 7,500 patients who are diagnosed with PKU, but who haven't sought out treatment at a clinic for at least two years.

BioMarin expects that Palynziq will be available commercially in late June at an average expected cost of $192,000 per patient per year. At that price, the company would generate $38.4 million in annual sales if it converts the 200 trial participants into regular patients and $480 million per year if it also successfully gets Palynziq prescribed to the 2,300 people being treated in clinics.�

Pricing isn't likely to be as high outside of the U.S., but the addressable market there is bigger, so an EU approval would also be meaningful.�EU regulators accepted Palynziq's application for approval earlier this year, and overall, management says there are 15,000 adult PKU patients in Europe and Turkey, including 4,900 who are being treated in clinics.

What's on deckKuvan's use in children should continue to make it a top-seller for the company, at least until generics become available. BioMarin has licensed rights to two generic drugmakers, and generic Kuvan could arrive�as soon as October 2020.

In the meantime, BioMarin will enjoy a dominant position in PKU that will help BioMarin take another step toward achieving profitability. Following Palynziq's OK, BioMarin has now won approvals for seven drugs. In 2017, the company's global revenue was $1.3 billion, so the potential to add hundreds of millions of dollars in new sales would significantly move the needle.�

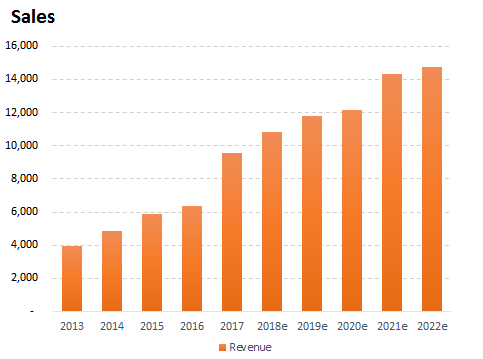

BMRN Revenue (Annual) data by YCharts.

In addition to improving progress toward profit, the additional revenue will also come in handy in support of BioMarin's R&D pipeline, including a potentially game-changing PKU gene therapy.�BioMarin hopes to begin human trials for a gene therapy that could restore the production of the missing enzyme in PKU patients in 2019.�The potential for a one-and-done gene therapy in PKU would significantly disrupt the market.

Overall, the impact Palynziq may have on BioMarin's financials in the next year or two, and the opportunity longer-term to create even better treatments for PKU, make it an interesting stock that I think is worth buying in growth portfolios.

Media headlines about Range Resources (NYSE:RRC) have been trending somewhat positive on Saturday, Accern Sentiment Analysis reports. The research group identifies positive and negative press coverage by monitoring more than twenty million news and blog sources in real-time. Accern ranks coverage of public companies on a scale of -1 to 1, with scores nearest to one being the most favorable. Range Resources earned a daily sentiment score of 0.07 on Accern’s scale. Accern also gave media headlines about the oil and gas exploration company an impact score of 46.3371462950661 out of 100, indicating that recent press coverage is somewhat unlikely to have an effect on the stock’s share price in the near future.

Media headlines about Range Resources (NYSE:RRC) have been trending somewhat positive on Saturday, Accern Sentiment Analysis reports. The research group identifies positive and negative press coverage by monitoring more than twenty million news and blog sources in real-time. Accern ranks coverage of public companies on a scale of -1 to 1, with scores nearest to one being the most favorable. Range Resources earned a daily sentiment score of 0.07 on Accern’s scale. Accern also gave media headlines about the oil and gas exploration company an impact score of 46.3371462950661 out of 100, indicating that recent press coverage is somewhat unlikely to have an effect on the stock’s share price in the near future.