Analysis of the model implies Lam Research (LRCX) is currently undervalued; resolute free cash flows will increase the intrinsic value of the business in the years ahead. Volatility in the industry will create opportunities for investors to acquire shares of Lam Research.

Use Volatility To Your AdvantageLam Research's stock price has been on a rough ride over the past few months, but a look at the company's future cash flow suggests that the stock has upside.

The semiconductor sector remains cyclical; it is for this reason that investors are wary, many believe we are at the end of that cycle and about to head lower with sales in the sector.

Currently, Lam blows through earnings estimates almost every time but that does not seem to be enough for investors. Regardless of what numbers Lam produce, investors cannot hold the stock over the previous all-time highs.

LRCX data by YCharts

Although no grim signs of the end of a cycle are near, it still gives investors a good enough reason to sell.

Lam has been a stock for traders as of late, producing regular swings of 20%. These fluctuations are great for traders who are trading either long or short. However, long-term fundamental investing in Lam Research should not be pushed aside, investors must be able to withstand the volatility and should be using it to their advantage.

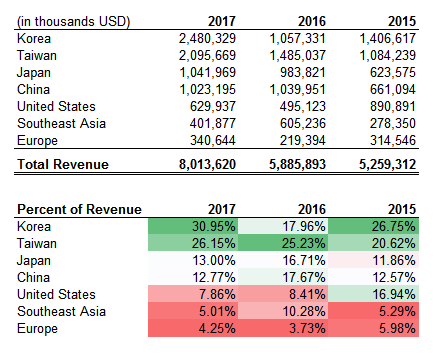

Asia Is A Key Contributor to Lam's Growth: Asian Fabrication Plants Continue To Scale

You can see above that Asia remains a core revenue driver for Lam, the U.S and Europe remain behind. Lam sells its products mainly to nations that rely heavily on cheap labor. The Asian area accounts for ~87% of revenue (as reported in the company's 10-K).

Local governments have shown great enthusiasm for supporting the semiconductor industry, and there has been a slew of policy support for related investment. - CCID Consulting, Asian Times

Lam Research creates and fabricates the tools for semiconductor manufacturing, including plasma, etch, photoresist strip, and wafer cleaning equipment.

The continued boom in the Asian semiconductor sector shows no signs of slowing. China wants to be more engaged in the chip space, this would conclusively lead to more revenue for Lam.

Several factories are set to kick off mass production this year, it's unclear how well they can perform in terms of yield and quality. Liu Kun, vice-general manager of CCID Consulting in Beijing.

Investment, in fact, is pouring into an industry which used to be dominated by the United States, South Korea, Taiwan, Japan and Europe. But that is changing rapidly. - Asian Times

Technology manufacturing, ultimately, produces jobs. The more non-government jobs that are available in an economy, the greater the GDP. China has ballooned its GDP to such heights over the years. But now, inevitably, growth is slowing. The push from the Chinese government to invest heavily in this sector could improve those GDP numbers.

Beijing will pump billions of dollars into semiconductor fabrication plants in a bid to overtake US, South Korea, Taiwan, Japan and Europe. - Asian Times

These days, everything requires chips of some sort and those chips will get cheaper very soon as competition heats up over in Asia. However, the competition in the semiconductor equipment making sector remains limited. This gives Lam Research a good opportunity to profit from such aggressive actions by the Chinese government.

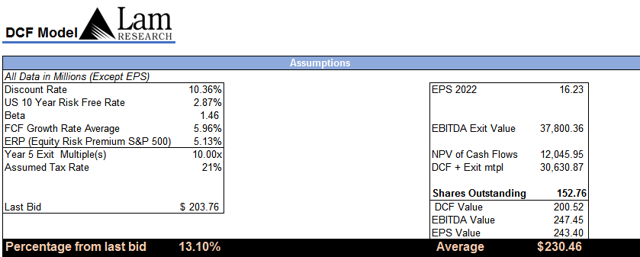

Earnings Model: DCF, EBITDA, EPSThe DCF shows a valuation of ~$200, while the EBITDA valuation shows a number of $247 - also included was the 2022 EPS of $16.23. In the model, we use an averaging of the results to come up with a fitting valuation.

The averaging of these numbers produced a share price of $230.46. The number is compatible with the performance of the stock and $234.57 remains the all-time high, this reinforces the analysis and assumptions in the model.

Source: Forecasts, Michael A. Ball. Historical data, Lam Research 10-K

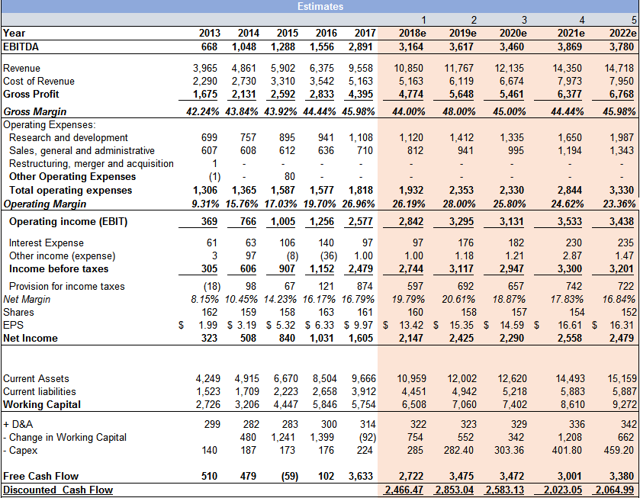

As we head forward in the year, the model will get updated and new outputs will get produced. We are only five months into the year and have more earnings to come from the sector, and this will impact the model going forward - this will more than likely produce a higher valuation number as earnings remain strong in the sector.

Capital expenditures were $49 million, which was down from $85 million in the December quarter. And as a reminder, we expect CapEx in 2018 will be higher versus 2017 levels to support manufacturing network expansion and growth in strategic R&D investments. - Lam Research Q3

The model above has a CapEx growth of 27% in 2018. Still, we see a good amount of upside in the implied share price produced.

The 2018 forward revenue number is just slightly above the real 2018 ttm revenue number of $10.29bln. Lam's management for next quarter are projecting $3.1bln, this would take the ttm revenue up to $11.05bln. The number already tops my estimate. Nevertheless, I remain on the conservative side and will update the numbers only when we get real data. Adding such numbers to the model now could make valuations appear too frothy - the sector needs to be verified for long-term growth before we can bump up numbers to inflate valuations more.

It is more than likely that Lam will beat its guidance on sales, they have a history of doing so. Looking at past performances and estimates, Lam has a high chance of hitting targets, but still keeping valuations on the conservative side guarantees investors keep a dubious head.

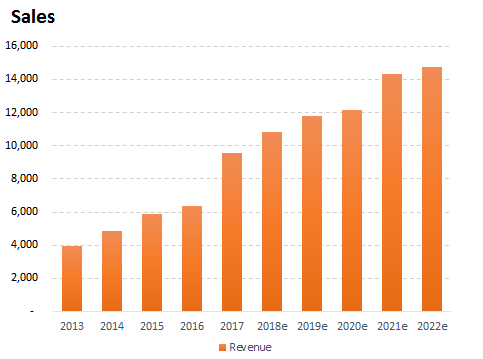

Source: Forecasts, Michael A. Ball. Historical data, Lam Research 10-K

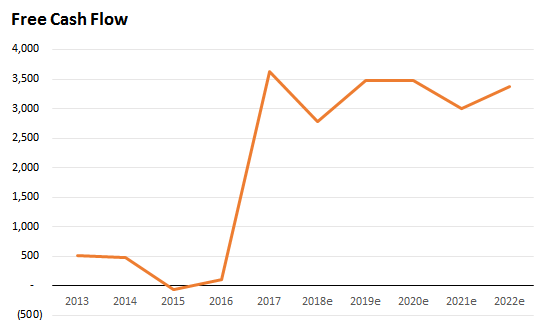

Sales should do great over the next five years. In the model for sales, we arrive at a 2022e of ~$14.7bln. The input keeps a relatively constant gross margin and growth rates average ~9%. In the model, the growth in sales does decline, starting off at 13% for 2018 and falling to 2.56% in 2022. The reasoning for the decline is to keep valuations on the conservative side as I said before. The model is merely to show a buying area and what the valuations could look like if we were to decline, it is not a target producing model as such.

Source: Forecasts, Michael A. Ball. Historical data, Lam Research 10-K

If we were to tweak the numbers and adjust the sales growth projections to that of the past, we would arrive at a higher share price estimate. Since the intentions of building this model are to support the long-term investor's current belief, it is always safer to depreciate forecasts than imply substantial growth regardless of what Wall Street is predicting. Even with such a decrease in sales growth, Lam looks undervalued; this is a good stock to own.

AI Could Boost Lam RevenueIntel's (INTC) recent investment in Syntiant implies that a large amount of competition in the sector is leaning towards AI, and Intel investing in Syntiant would be a wise option rather than trying to compete.

Syntiant has a comparative advantage, and Intel is already introducing Syntiant to more than a dozen companies that could be using their chips. The AI market is starting to get noticed and products are becoming more mainstream.

As Lam is only one of a few semiconductor equipment makers who dominate that space, this gives Lam an advantage of being central to a potential AI boom. Lam could be significant in producing the equipment for these new and emerging companies.

Recent Upgrades

Source: Tipranks.com

Cowen resumes Lam Research at 40% upside Lam Research +1.5% on Citi upgrade Analysts say buy the dip in Lam Research despite lower shipment guidanceAll the targets issued are above current levels, this should reinforce the longer-term investor's outlook regardless of the volatility.

Analysis ConclusionI would be happy adding Lam shares all the way up to $230 before I grow skeptical. We are still in limbo about the cycle. People are predicting the cycle will remain on an upswing, but we need to remain conservative in our valuations. Some prominent investors are saying that we are at peak cycle and they are reducing Lam shares. Once we get a confirmation about the sector, then we can issue targets and improve the model.

I predict that the cycle has a few more years left yet, but volatility will remain for a few more quarters. It would be wise to maintain a position in Lam, buying on any -3% days. We have seen such days over the last few months even after a blowout earnings - just a day or two after the stock sells off, it rebounds. The good news is that Lam is way below that $230 price the model implied.

Lam reports their next quarterly results on the 25th July and the market is expecting ~$5 EPS.

Disclosure: I am/we are long LRCX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment